The Focus - Our Tax E-Newsletter |

Records Retention Best Practices

Now that we are half way through the 2023 tax year, we should consider cleaning out our old records to prepare for the next tax year.

The biggest question is what am I required to keep and for how long? If I get audited what records will I need to provide to the auditor? You must first consider what the IRS wants you to keep and for how long.

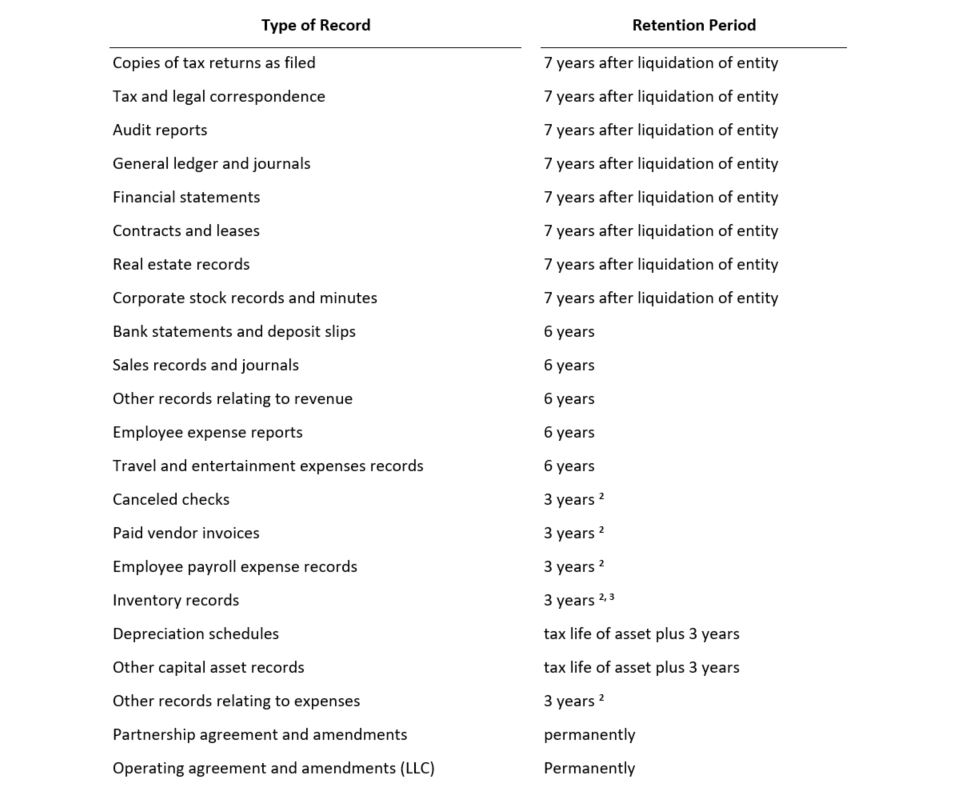

Below is a list of the recommended document retention periods. It may be necessary to retain some records longer because of nontax reasons. For example, insurance policies, leases, real estate closing statements, and employee payroll records might need to be kept longer than needed for IRS purposes. You should consult with your attorney about how long to retain legal documents.

Recommended Document Retention Time Periods:

There is no required format for keeping records except that they must be readily available. If files are stored electronically any software needed to access the files also needs to be kept current and available. The IRS has also issued guidance on using electronic storage systems to satisfy record keeping requirements. An important part of any document retention policy is compliance with Internal Revenue Service requirements. All businesses and individuals are required to keep books and records that support the amount of gross income, deductions, as well as credits claimed on the taxpayers' income tax return. At a minimum these records must be retained until the expiration of the statute of limitations expires.

The statute of limitations period for income tax returns is generally three years. However, it's six years if there is a substantial understatement of gross income (i.e., the return understates income by more than 25%). The statute never runs if a fraudulent return is filed or if no return is filed. Therefore, a good rule of thumb is to add a year to the statute of limitations period. Using this approach, you should keep most of your income tax records a minimum of four years, but it may be more prudent to retain them for seven years. However, be sure to consider applicable state tax statutes since they may include unique record retention requirements.

These guidelines are disregarded in light of pending legal action or audit. The Tax Court has punished taxpayers that destroyed records when the destruction was not in the ordinary course of business and was done before the records were required for audit or litigation purposes.

Document destruction is as important as the storage of documents. Paper documents that contain confidential or sensitive data should be shredded using a secure system. Electronic documents are destroyed by deleting them from the medium on which they are stored and then purging the medium itself.

Please contact your Dermody, Burke & Brown advisor if you would like to discuss any of this information in greater detail.

The information reflected in this article was current at the time of publication. This information will not be modified or updated for any subsequent tax law changes, if any.